Vertex 2026: notes from the vSaaS world

400 vSaaS and fintech founders, operators, and investors all in one room: the SaaSpocalypse is overblown, great fintech is still early, and the moats are quietly moving to the places AI can't touch.

400 vertical software and fintech founders, operators, and investors met in New York last week for Rainforest’s Vertex conference. Everyone from public-company fintech GMs to growth-stage operators to early-stage founders. Companies building for spaces as diverse as construction, field services, legal practices, dental offices, restaurants, and laundromats.

Despite the barely-shared vocabulary, I kept hearing the same language. Lots of talk about the SaaSpocalypse and why it’s overblown. How AI is an accelerant when you own the system of record. How much room embedded payments still have to run. And more. Here’s a recap of what I learned.

What SaaSpocalypse?

The AI discourse has been writing SaaS off for months. Seat compression. Zero-marginal-cost competitors. Vertical was supposed to be especially exposed because it’s “just” workflow software.

The strongest AI work in vertical isn’t being marketed as AI. A vertical ERP that parses every unstructured customer email into the CRM is sold as a better ERP. A field service platform that generates quotes from a voicemail is sold as a faster estimator. The software gets smarter around the customer, and the customer uses more of it, not less. Nobody I talked to was seeing AI drive churn, and many were seeing it drive acceleration.

Trust is the new taste

Horizontal software loves to talk about taste as the differentiator. In vertical, it’s trust. These customers have been sold software for years by vendors who over-promised and under-delivered, and the new wave of agentic point solutions is hitting the same wall of skepticism.

Trust looks different than taste. It’s the vertical-specific brand that tells an HVAC owner you understand HVAC, rather than a generic tech logo that happens to serve field service. It’s showing up at the industry’s trade shows, ride-alongs, and shop floors rather than waiting for customers to come to you. It’s training everyone in your company (especially customer support and sales reps) on the customer’s industry, not just on your product. Taste wins the demo. Trust wins the renewal, the referral, and the second product line.

Embedded payments is huge (and just getting started)

The conventional wisdom on embedded payments has hardened. Most platforms have shipped it, take rates are compressing, and the easy money is behind us. Vertex was a useful corrective on all three. The founders who have been at it longest were the most bullish, not the least. Payments has a lot of room left. Most platforms aren’t close to their ceiling.

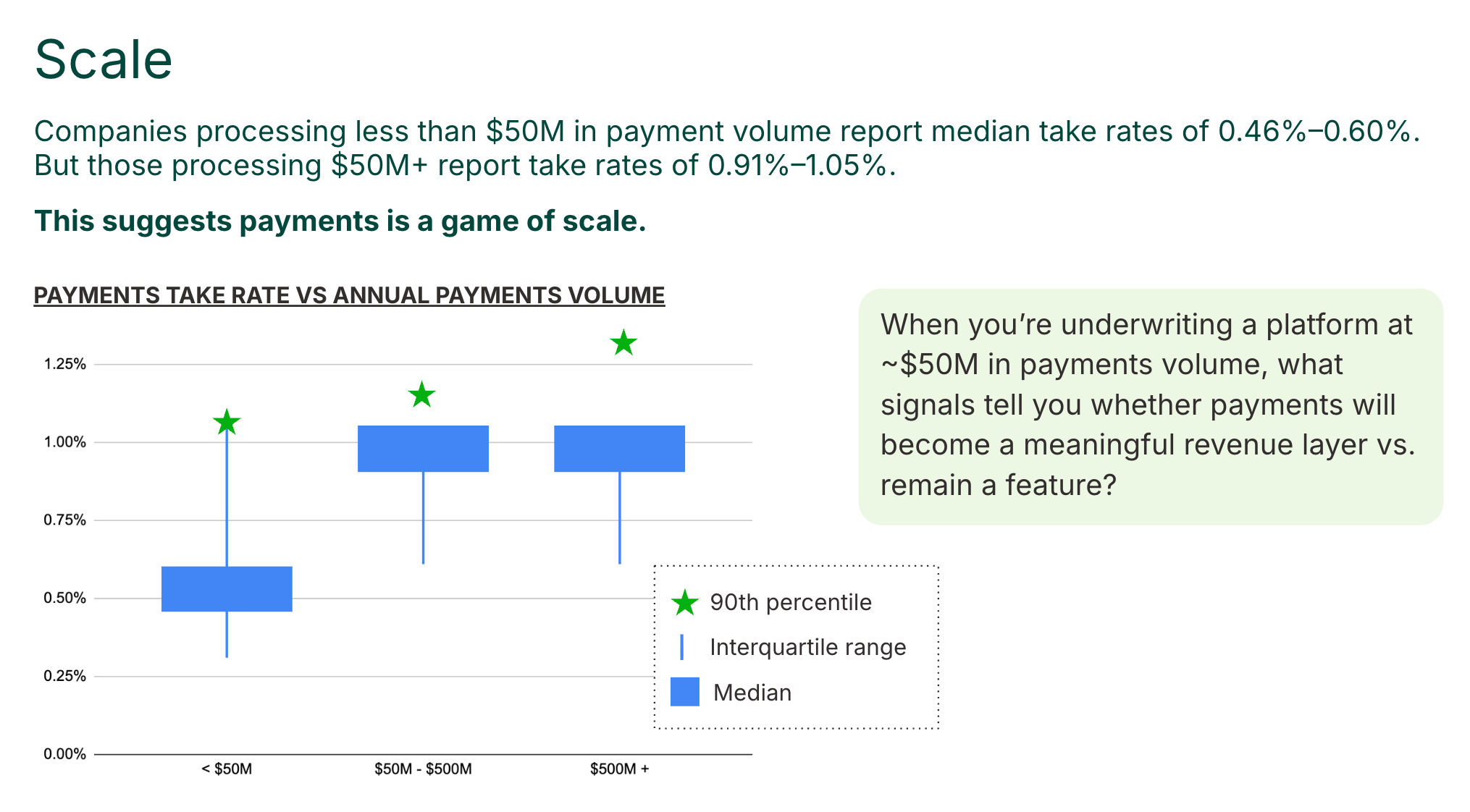

Start with take rates. The “compressing to zero” narrative is overstated. Nearly half of companies in Rainforest’s 2026 embedded payments benchmark report take rates above 90 bps. And when a platform grows from less than $50M processing volume to $250M+ volume, the median take rate doubles (0.46-0.60% below, 0.91%-1.05% above). Payments is a game of scale, and the thresholds where the economics inflect are closer than most platforms realize.

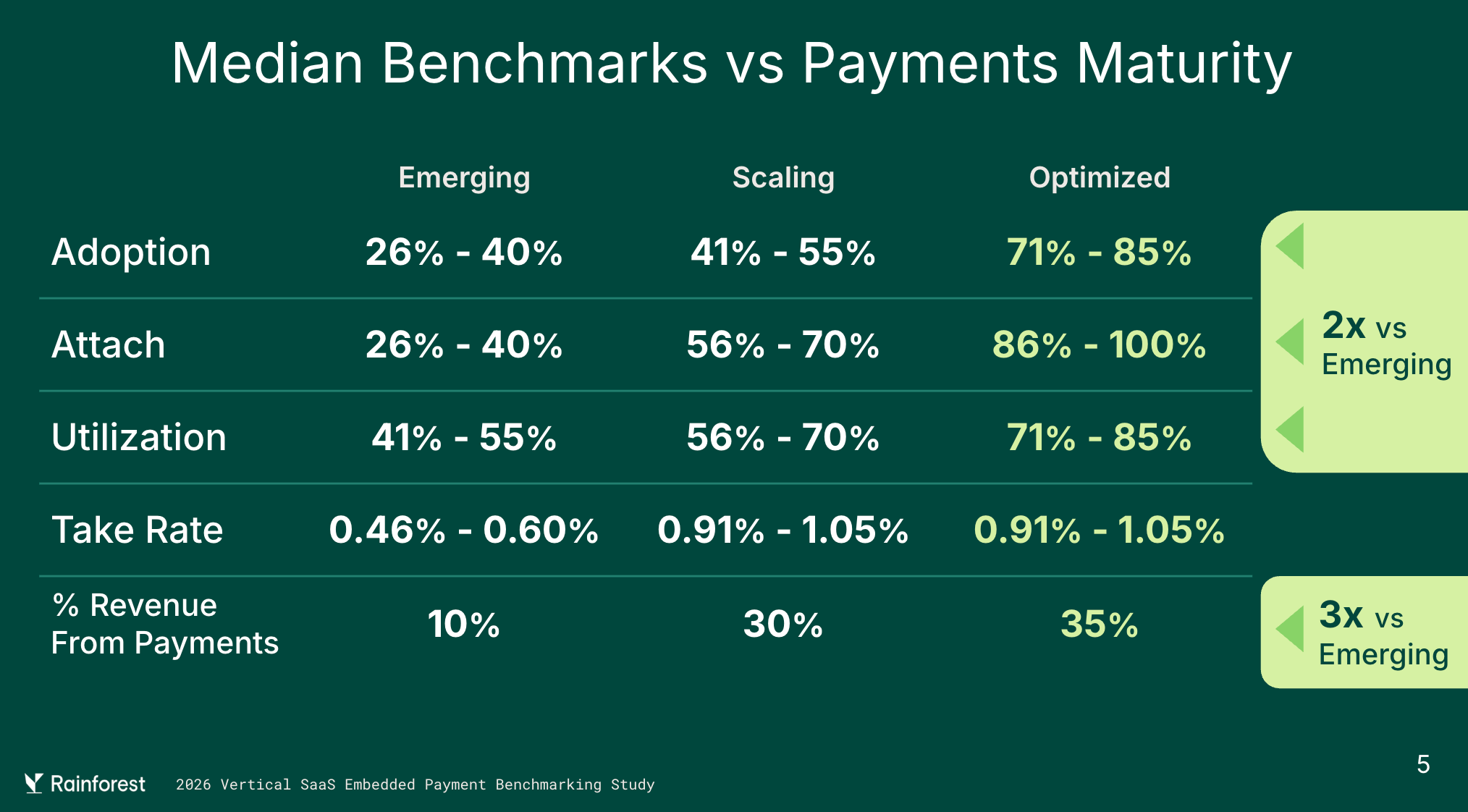

Then look at how much room is left even at maturity. Median share of revenue from payments peaks at 3-4 years after launch (35%) and dips slightly at 5+ years (30%). The tempting read is natural maturation. But split the 5+ year cohort into “Scaling” versus “Optimized” and the dip is concentrated in the Scaling group. The Optimized cohort keeps compounding past year five. The long-tail dropoff isn’t gravity. It’s the companies that quietly reallocated attention somewhere else.

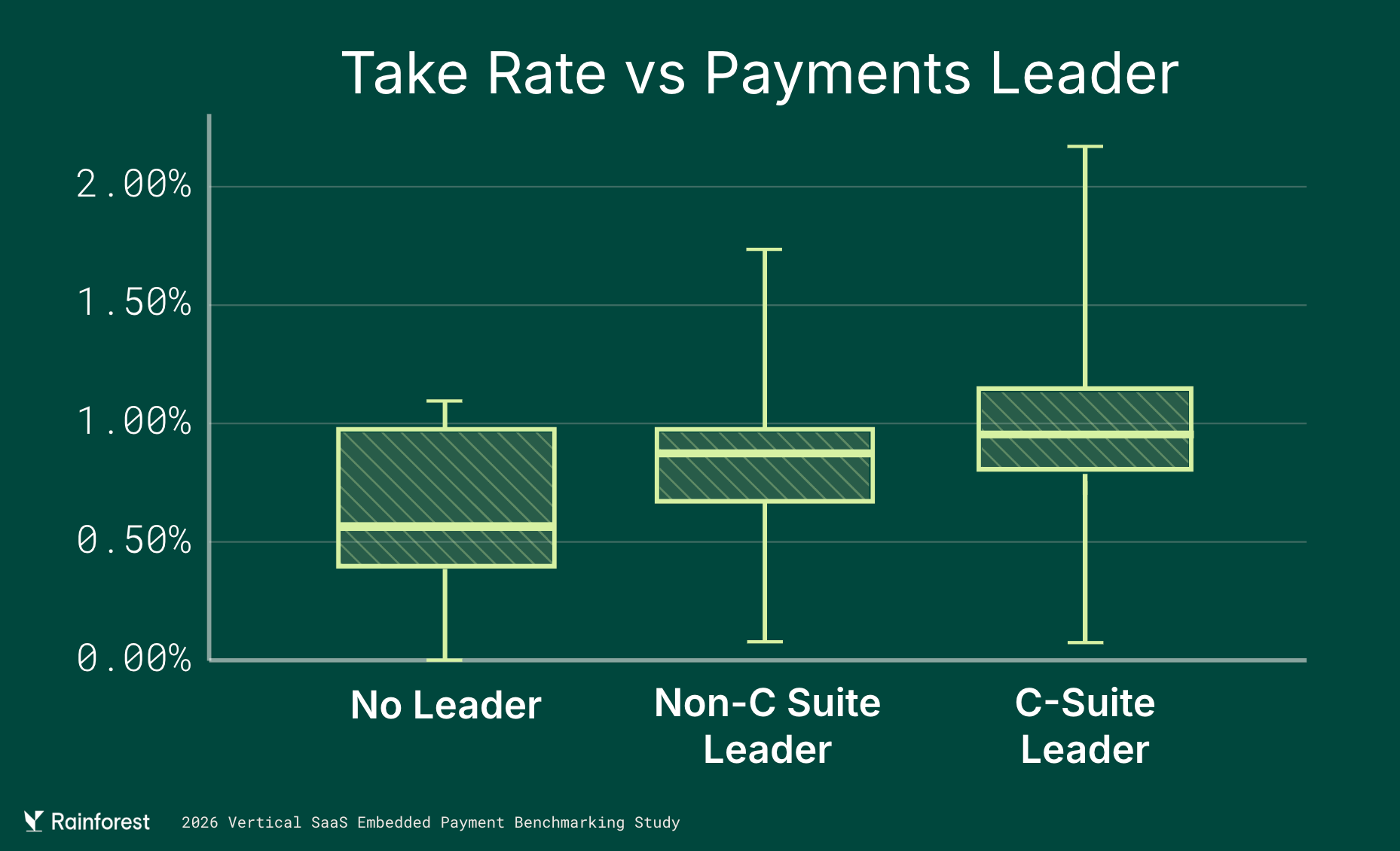

The leadership data tells the same story. Companies with a C-suite payments leader post almost 2x the take rates of those with a no-leader. Take rate, attach, and revenue share don’t drift upward on their own. They respond to scale, focus, and ownership. The platforms that keep treating payments as a serious product line will keep finding growth in it long after everyone else has moved on.

The winning AI is less agentic than you think

The AI discourse assumes the endpoint is full automation. The founders selling to contractors, clinics, and shop owners don’t agree. The teams winning here are designing for a spectrum. An AI voice answering service that routes to a human on the first hint of complexity. An agentic AP workflow that auto-posts low-risk vendor bills and kicks medium-risk ones to an accounting clerk. A scheduling tool that drafts the reply and makes the owner hit send.

What makes these products work isn’t how much they automate, but how cleanly they hand off when they shouldn’t. Customers choose their comfort level, and the trust compounds every time the product respects the choice. The calibration is doing the work, not the autonomy itself.

Context graphs are the moat vertical software already built

Every AI product is chasing context, and vertical software has been quietly building vertical-specific context graphs for years. The schema of a restaurant’s menu, modifiers, kitchen stations, and labor model. The workflow of a law firm’s matter, phases, timekeepers, and trust ledger. The relationships on a construction project between job, cost codes, change orders, and retainage.

That structured data is the substrate AI needs to be useful, and vertical software already owns it. AI makes software itself cheaper to build, which pushes the moats toward the hard things AI can’t touch. Proprietary context. Regulatory relationships. Hardware integration. The messy physical world these companies live in.

Embedded grows up

A couple of years ago, the embedded narrative was peak hype. Platforms were integrating embedded providers left and right on the assumption that anything embedded would compound. That first wave underdelivered: integrations underperformed, embedded products were thinner than they looked, and many ended in awkward unwinds.

Platforms got pickier. The bar is higher, vetting is tighter, and second-tier partners are getting displaced. The embedded providers themselves have used those years to grow up. The new generation is more honest about what it does and doesn’t solve, and more valuable to platform customers. Established categories are maturing (e.g., accounting with Tight and Layer, lending with Kanmon, payroll with Check and Salsa), and emerging categories are getting serious heat (e.g., embedded marketing with Reach, embedded voice with Dialstack).

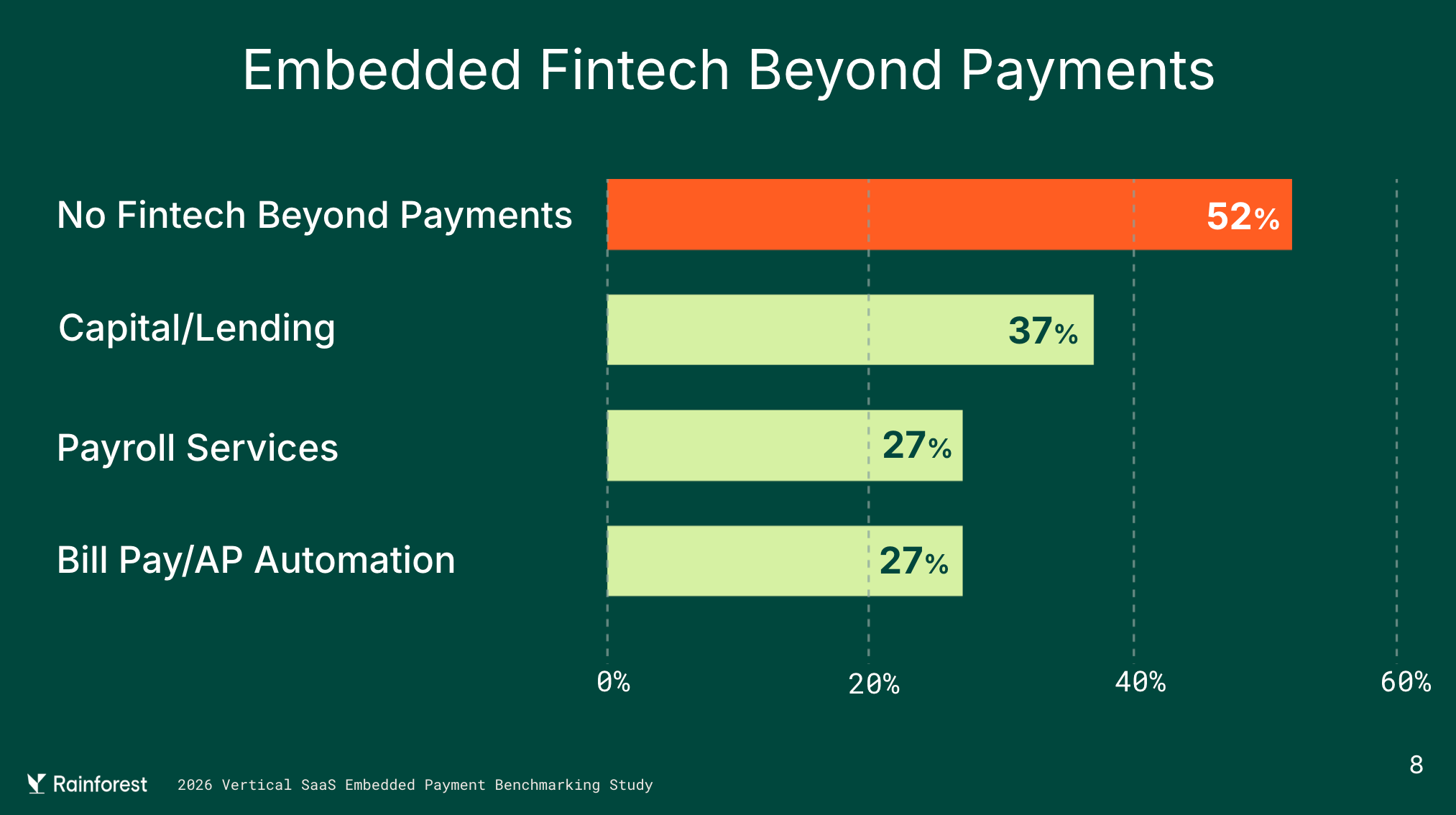

And the surface area is still largely unbuilt. 52% of vertical software companies in the study have no embedded fintech beyond payments at all. The ones that do cluster in capital/lending, payroll, and bill pay. Plenty of runway, just not for anyone showing up with a checklist.

Vertical software has developed its own gravity. The businesses differ wildly on the surface. Restaurants don’t look much like law firms, and neither looks much like a wellness studio or a construction GC. But the playbook is shared, and shared freely. At most conferences, every conversation is competitive. At Vertex, most conversations were comparative. The category is still early enough that the pie is growing faster than the fight for it.

My name is Matt Brown. I’m a partner at Matrix, where I invest in and help early-stage fintech and vertical software startups. Matrix is an early-stage VC that leads pre-seed to Series As from an $800M fund across AI, developer tools and infra, fintech, B2B software, healthcare, and more. If you’re building something interesting in fintech or vertical software, I’d love to chat: mb@matrix.vc